I will respond to your first post eventually. I think that the problem is that I haven’t given an adequate definition of “2nd order value” or whatever.

I’ve been listening to Human Action on audiobook (doing this is pretty awful; I don’t recommend), and one general point it makes is that we need to be careful to frame all our discussion of “value” in terms of subjective value. Things can only be of value to an individual. I definitely wasn’t doing this. Neither were you, in e.g. this sentence:

Anyway,

What is a BTC “fan”? I assume that by fans you mean people who value bitcoin? If so, then the “fans” include almost everyone (including you, since you’d be very happy if someone sent you 10000 BTC), so your hypothetical is much stranger than it first appears.

Are you imagining like, everyone dies except one person, then concluding that the one remaining person would not value BTC? That’s true, but such an argument would also basically apply to gold: if everyone but me disappeared, a pound of gold would probably be less valuable to me than e.g. a pound of rice.

I mean someone who subjectively values bitcoin outside it’s use as money. if someone offered to pay me in BTC, I’d consider it, but i wouldn’t necessarily keep it in BTC. I consider ‘fans’ those ppl who’d bias BTC particularly (above other crypto or other methods of holding value). I’m not a fan, in that I’d only hold it for pragmatic reasons. Does that make sense?

No. I don’t think either of these definitions are sufficiently precise, since e.g. I couldn’t use them to determine whether or not I am a btc fan.

I value BTC, but do I value it “outside of its use as money”? I have no idea what that would even mean, all I know is that 1 BTC is worth like $50,000 USD right now & so BTC is quite valuable to me.

Am I a person who would “bias BTC particularly (above other crypto or other methods of holding value)”? I have no idea what this means. Are you imagining some hypothetical scenario where 1 btc has the same value as 1 eth or 1 dogecoin or 1 of any other cryptocurrency, then defining a fan as someone who would prefer to have 1 BTC instead of 1 of another cryptocurrency in that scenario?

I think we might be getting away from the point. The reason I introduced the idea of fans was to say: the fact some some die-hard core audience exists now isn’t a reason think that BTC will maintain a nonzero value. The nature of that audience isn’t too important, just that it’s not a good argument that BTC will maintain value.

I think that part of the reason why I was probing into your definition of fans is that it’s not clear to me that BTC actually relies on anything like a “die-hard core audience” in order to maintain value.

right now, it doesn’t. There’s lots of other reasons that it has value, at the moment. But if that went away, and there was no die-hard audience, why would it ever recover?

We don’t know how cheap and easy transmutation will get.

Also, since you guys don’t seem to be making a tree, or doing anything else related to CF (including no post mortem on the communication point I raised), the discussion is a bit off-topic.

Okay yeah, we should make a discussion tree. Besides being off-topic, I think the conversation between @Max and me was getting overwhelmingly complex/long.

I made a rough draft of a discussion tree which I think summarizes a big part of our conversation. The root of the tree is the claim that we are trying to refute. The nodes directly underneath the root are attempted refutations of that claim, the nodes underneath those are attempted counter-refutations, etc. I tried to reduce everything to essentials. Here it is:

In the long run, the value of BTC will NOT go to ~0.

Continuity matters. If something disrupts the network of BTC miners for—say—100 years, there is no good reason to think that people would stick with BTC.

If BTC still has value after a 100 year disruption, then miners will still have an incentive to mine it. Therefore, the reason to stick with BTC only goes away after a disruption if the value of BTC also goes away after a disruption. In other words, the argument in the node above is circular: it assumes that the root of the tree is false.

BTC doesn’t have any value as a commodity, so there’s nothing to stop demand for BTC from going to zero.

The first clause of this sentence is false. Although BTC has far fewer uses as a commodity than gold, BTC actually does have some value to people as a commodity, because BTC is already valuable. E.g. someone could use his BTC to flaunt wealth.

Are there any parts of this tree that you don’t like or don’t accept, @Max?

Yeah, I think I did take my own context for granted. I was watching the episode at the time with a friend (it was released sometime that day). The other major factors that occurs to me is that I wasn’t sober, and was eager to post given its relevance.

I agree that it’s an important error, generally.

In this case I feel like it’s not a big deal, tho. Mb that’s part defensiveness, or trying to ‘brush it off’, so I’ll share my reasoning. The post is atypical in that: I usually think about my posts here before making them (draft them, etc) and didn’t that time; I was unusually eager to post it (like, I felt like it was time-sensitive to post it b/c the ep was recent); and I wasn’t sober. So, since it’s atypical, my intuitive reaction is that I don’t need to worry about making that mistake again (for similar-enough cases) provided I keep a better check on when I post and my motivations for posting.

That said – and this isn’t the first time I’ve noticed this pattern – I did consciously consider beforehand if I should say more or post at all, but posted anyway. in this particular case, I thought more about not giving away spoilers than context tho, which is (I think) part of why I didn’t add more context – but those two things (context and spoilers) aren’t related. Like it’s fair to omit why it’s relevant (tho we do have spoiler tags), but not to omit which episode I’m talking about.

I know I’ve made this sort of mistake outside CF though, even without all the above excuses. I don’t think it’s been v common, but I haven’t been watching for it before now.

IDK if I’ll end up looking through past posts for that sort of mistake, but it is something I am going to watch out for, esp considering that I know I’ve made similar mistakes before.

I did mention the tree before the south park post, not sure if you saw that. I agree that we’re not really sticking to the make-a-conversation-tree plan, though.

(Note: not sure exactly why, but my reply got posted to the crypto currency fraud thread instead of this one; copying it here)

Yeah – I didn’t think you’d answered it (I probs should have mentioned that).

The post you linked has problems IMO; not sure if you consider them relevant or not to the discussion, though.

Bitcoin isn’t dead between blocks – there’s no way for it to be alive without gaps, so logically it can’t be dead in those times. There is still an ongoing process – miners are hashing – but the results of that process are stochastic (next block could be in 20 seconds or 20 minutes).

The above is one reason, but another is that there’s a sense of financial continuity – but that wouldn’t necessarily be the case 2, 20, or 200 yrs later. I don’t think we need to agree on that much here btw, like roughly day-to-day continuity is enough (e.g., stock markets often close overnight, so it seems like day-by-day continuity is good enough for most finance stuff).

Yes, tho I’m not sure if the nodes correspond to each of our points or not. If each node is either something one of us claims or something we agree/disagree on, then I don’t necessarily disagree with the nodes.

Two points of disagreement are below, but this gives me an idea for a cycle we could go through to build the tree, taking turns as we build out each branch:

Given there’s a prior node, one of us interrogates that point. The goal of that person is to figure out the next node(s) in the tree, for that branch. The idea is that having little discussions about each point let’s us both get a good understanding for the main through-line of that branch.

Once the interrogator is satisfied (and the arguments are understood), a node is added, and the roles swap.

So the next step for me would be to figure out follow on nodes for the two depth=2 nodes (taking root at depth=0). It seems like you own the root node, then I own d=1 nodes, and you own d=2 nodes (in your tree). That’s part of what I’m basing the above on.

Things in the tree I disagree w/ depending on what the nodes correspond to:

(Note: Emphasis mine)

I disagree with this b/c we’re talking about something over time. Referring to the past doesn’t necessarily mean the argument is circular.

IMO flaunting wealth isn’t a thing BTC does b/c it is or isn’t a commodity – it’s a property of BTC as an economic good. Cash is the same – flashing cash isn’t flaunting wealth for anything to do with its material (paper, polymer, w/e). Similar with gold. Basically, flaunting wealth is only possible b/c the good only has prior value due to it’s properties as an economic good (i.e., a money-like thing).

I disagree with what you write below this, but we shouldn’t talk about this post directly because the point I’m making in that post is already contained in the discussion tree (but in a cleaner / more applicable form). We should focus on the discussion tree.

I have new thoughts about this part of the conversation tree:

I thought of a counter-counter-refutation. (edit: what I’m about to say has a lot in common with the point made in this post but I forgot about it until now).

BTC does indeed have this “second order” value coming from the fact that it’s already valuable (see the quote above or this post), but it occurred to me that as the price of BTC decreases, BTC will have less and less “second order” value. A corollary of this is that for a rational market actor who is not a speculator, his demand for BTC will decrease as the price of BTC decreases. I know of no mechanism that would cause the price of BTC to naturally* go back up if it goes down, so therefore** I expect the price to decrease to zero in the long run.

Contrast BTC with gold, which has “first order” value (it looks pretty, it can be used in high-end electronics, etc), in addition to having “second order” value. If the price of gold goes down, its “second order” value goes down, but its “first order” value is unaffected. For a rational market actor who wants to use gold for “second order” purposes, his demand for gold will decrease as the price of gold decreases; but for a rational market actor who wants to use gold to make things, his demand for gold will increase as the price of gold decreases. I suspect that these two forces roughly balance each other out in the long run.

TL;DR the discussion tree looks like this now:

In the long run, the value of BTC will NOT go to ~0.

Continuity matters. If something disrupts the network of BTC miners for—say—100 years, there is no good reason to think that people would stick with BTC.

If BTC still has value after a 100 year disruption, then miners will still have an incentive to mine it. Therefore, the reason to stick with BTC only goes away after a disruption if the value of BTC also goes away after a disruption. In other words, the argument in the node above is circular: it assumes that the root of the tree is false.

BTC doesn’t have any value as a commodity, so there’s nothing to stop demand for BTC from going to zero.

The first clause of this sentence is false. Although BTC has far fewer uses as a commodity than gold, BTC actually does have some value to people as a commodity, because BTC is already valuable. E.g. someone could use his BTC to flaunt wealth.

The type of value described above decreases with demand, so it does not protect demand for BTC from going to zero.

*What do I mean by “naturally”? Something like, a price goes up naturally if something other than peoples’ ignorance caused it to go up.

**I just wanted to note that this “therefore” is not even close to being obvious. It’s hiding a pretty complicated argument and some extra assumptions, which I spent a long time trying to write out but ultimately deleted because what I wrote was bad and unnecessary.

Yes. Early on in Bitcoin’s history this was brought up – e.g., if you tried to sell a house then buying ~$1m of BTC to do that would move the market significantly, and similarly cashing that $1m out all at once would do the same, too.

You put it more generally, but I think the essence is the same.

Have you changed your mind?

There’s one special case I can think of where BTC might go back up – if it were the only option; if no other cryptos existed.

I didn’t understand this when I first read it. I thought I did. I agree with it now.

The “continuity matters” node assumes that something bad happens and BTC → 0, and uses the lack of an exchange value to argue that ppl wouldn’t adopt it again, so BTC would stay at 0.

I agree it’s circular. Another decisive crit I thought of is that: whether BTC could recover from going to 0 is a different issue to whether BTC will or will not go to 0.

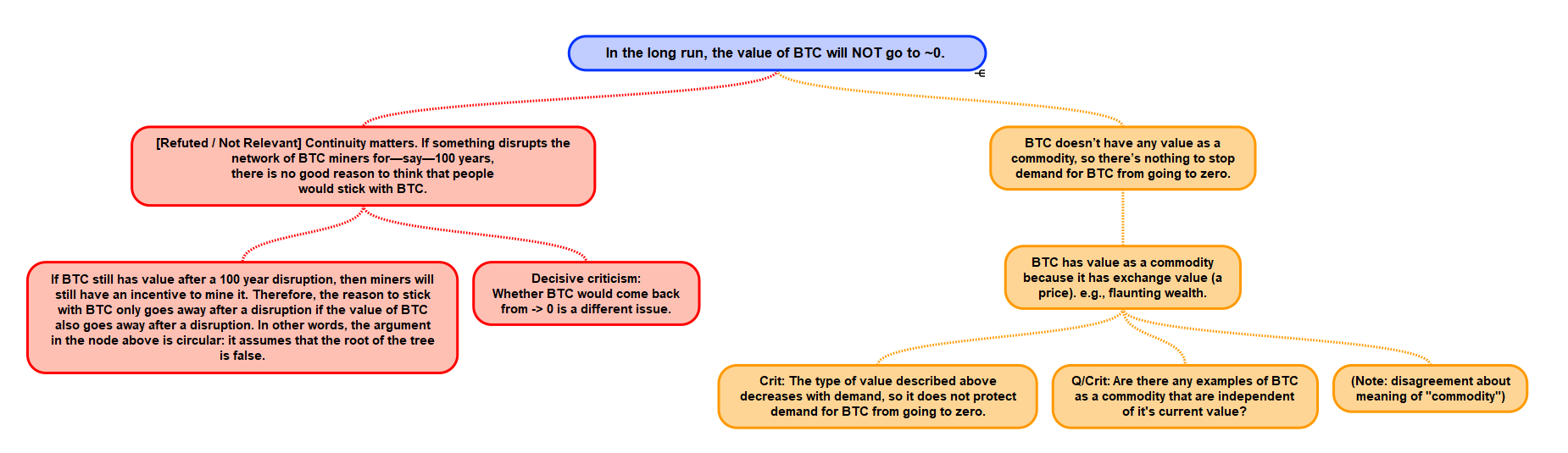

I recreated the conversation tree based on yours with some added nodes.

In the long run, the value of BTC will NOT go to ~0.

[Refuted / Not Relevant] Continuity matters. If something disrupts the network of BTC miners for—say—100 years, there is no good reason to think that people would stick with BTC.

If BTC still has value after a 100 year disruption, then miners will still have an incentive to mine it. Therefore, the reason to stick with BTC only goes away after a disruption if the value of BTC also goes away after a disruption. In other words, the argument in the node above is circular: it assumes that the root of the tree is false.

Decisive criticism: Whether BTC would come back from -> 0 is a different issue.

BTC doesn’t have any value as a commodity, so there’s nothing to stop demand for BTC from going to zero.

BTC has value as a commodity because it has exchange value (a price). e.g., flaunting wealth.

Crit: The type of value described above decreases with demand, so it does not protect demand for BTC from going to zero.

Q/Crit: Are there any examples of BTC as a commodity that are independent of it's current value?

(Note: disagreement about meaning of "commodity")

Additions:

I think we’re using different meanings of “commodity” – mine doesn’t include 2nd order value (which I equate w/ the idea of an economic good with exchange-value from TMC). We might not need to resolve this, considering your crit and the next node.

I have a question that I think needs to be answered for “BTC has value as a commodity” to be true considering your crit: Are there any examples of BTC as a commodity that are independent of it’s current value? If we don’t have an answer to that (or the answer is “no”), then I think we should mark these nodes refuted and/or not relevant:

lmf’s tree: “BTC actually does have some value to people as a commodity, because BTC is already valuable. E.g. someone could use his BTC to flaunt wealth.”

My tree: “BTC has value as a commodity because it has exchange value (a price). e.g., flaunting wealth.”